With the S&P 500 piercing through the 1,400 level for the first time since the recession, it is getting harder for value investors to find bargains. Consumer-oriented growth stocks, in particular, have seen their share prices and valuations soar during the current bull market. Restaurants like Chipotle Mexican Grill (CMG) and Panera Bread (PNRA) as well as clothing companies like Lululemon (LULU) and UnderArmour (UA) have become market darlings, with P/E ratios stretching into the 30's, 40's and even 50's. Bargain seekers need to dig deeper to find attractive stocks if they want to avoid paying 2-3 times market multiples for their stocks.

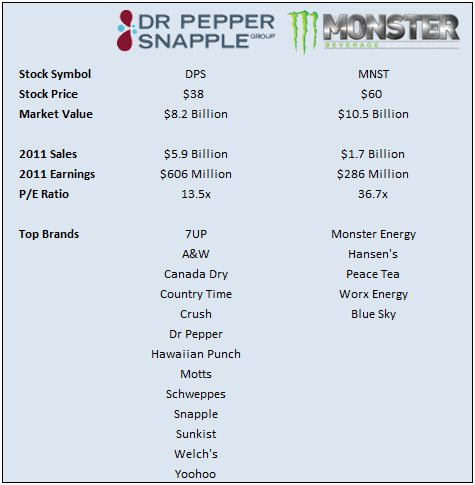

An interesting dichotomy has arisen in the beverage space, which to me is a great illustration of how the bull market has played out in recent months. A blue chip beverage company like Dr Pepper Snapple Group (DPS) has lagged in the recent market rally, whereas the smaller, faster growing Monster Beverage Corp (MNST) has soared. In fact, despite being three times the size of Monster in terms of sales, Dr Pepper Snapple is actually valued at more than $2 billion less on the public market. Below is an interesting comparison of the two companies and their stocks.

Now, given that MNST is a smaller company and as a result is growing faster, I would not argue it should not trade at a premium to DPS, but this much of a premium seems a bit out of whack. If I was investing in a set of brands, I would choose DPS in a heartbeat. And the fact that I could get three times the revenue for a cheaper price would be icing on the cake.

In this current market, I suspect MNST shares are overvalued and DPS is undervalued. The energy drink market is growing faster and is more of an exciting growth story for investors, whereas the DPS brands, while prolific, only grow at the rate of GDP globally. As I try to find bargains in an overbought (my personal view) stock market, I am gravitating towards stocks like DPS. Not only do they look fairly inexpensive on a valuation and brand equity basis, but the value is even more apparent when they are compared with some of today's hottest consumer companies.

Full Disclosure: Long DPS and no positions in CMG, MNST, LULU, PNRA, or UA at the time of writing, but positions may change at any time