I wanted to pass along some excellent work by Gary Townsend of Hill-Townsend Capital on how there can be such a hot debate on Wall Street about the solvency of our nation's large banks. Essentially, it comes down to this: if you take loans on bank balance sheets and mark them to market, you can show that the bank is insolvent. Of course, bank loans held for investment are not marked to market according to GAAP (instead loan loss reserves are set aside over time to cover future losses), but why let some silly accounting rules get in the way of bank solvency analysis!

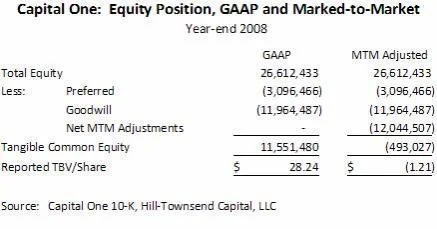

Here is a graphic put together by Townsend to illustrate how a bank (in this example, Capital One, a Peridot holding coincidentally) can be very solvent under GAAP but insolvent if you mark every loan on its book to market.

Gary comments on the data above by adding the following:

"So with full-bore MTM treatment of Capital One's balance sheet, after net MTM adjustments of just over $12 billion, the company's tangible book value of $28.24 per share falls to minus -$1.21. There are innumerable other examples.

The point is that the market takes Capital One's MTM disclosure, does the math, and values Cap One as if the loans were marked to market anyway. That's how Capital One and many other banks are well-capitalized according to GAAP and regulatory standards, but insolvent in the view of many market participants. GAAP results become irrelevant. And it's how Roubini and others come up with their huge loss numbers, on their way to declaring the U.S. banking system insolvent.

The problem, of course, is that the MTM results have little to do with the intrinsic value to a bank of a loan or a security that it plans to hold to maturity. In a bank, the decline in a loan's value is offset with a forward-looking provision for loan losses. The decline in the loan prices net of loan loss allowances is not due to credit deterioration; it's the result of the distortions and speculation in the world's financial markets. Mark-to-market accounting isn't improving the transparency of bank accounting. It has reduced it, with enormous and growing damage to our economy and prospects."

Full Disclosure: Peridot Capital was long shares of Capital One at the time of writing, but positions may change at any time