As you may have already read in Business Week's 2009 Investment Outlook issue (dated 12/29-1/5), I highlighted the recently formed Anheuser-Busch InBev (AHBIF) as a potentially attractive bargain pick. Despite various other mergers failing to get done in the current credit environment, Belgium's InBev paid $52 billion in cash to acquire Anheuser-Busch. Fearing that borrowing the money to get the deal done would prove overly aggressive, InBev's stock simply cratered in the months leading up to the deal, and shortly after it was completed.

In addition to the plan to borrow the entire $52 billion, InBev's plan to repay $10 billion of that loan right away via a rights offering proved much more ominous than once thought. With InBev's stock price collapsing (the stock peaked at US$95 and fell all the way to US$14), the number of new shares needed to be sold to raise $10 billion of capital greatly increased. In fact, InBev sold about 1 billion new shares which was far greater than the 600 million shares outstanding before the buyout. All of the sudden, InBev shareholders were diluted by more than 60%, which was a main reason why the bottom fell out of the stock shortly after the buyout was completed.

While the dilution certainly was much more than anyone expected, the business prospects for the combined company have not really changed, which is at the heart of why I think there is a good chance they can actually pay back the loans successfully. Beer sales worldwide are not going to be dramatically affected by the global recession and lower commodity prices could even help boost margins as input costs decline.

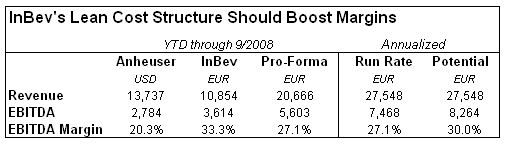

Through the first nine months of 2008, Anheuser-Busch was on pace for annual EBITDA of about $3.9 billion, with InBev tacking on another 5 billion euros. That comes to nearly 7.5 billion euros of annual EBITDA before accounting for any cost synergies. Assuming the A-B portion could see an improvement in profitability due to cost cuts, there is reason to think the combined company could have annual EBITDA of more than 8 billion euros. To see how I get to that number, I have included the following chart:

Comparable large, dominant, global beverage brands fetch about 10 times cash flow in the public markets so an enterprise value of 80 billion euro is not an unreasonable valuation in my eyes. The catch, of course, is the tremendous debt load InBev took on to become the most dominant beer company in the world.

The companies had more than $7 billion in net debt before the transaction. Even after 20% of the $52 billion load is repaid with proceeds from the new stock sale, Anheuser-Busch InBev remains saddled with about 40 billion euro of net debt, which accounts for half of the projected enterprise value of the company. At the current point in time, that translates into a little more than $24 per AHBIF share. After rising from a low of $14 in recent weeks, the stock trades in the low 20's already.

Is there any upside left then? Well, leverage works both ways. If you take on too much debt and your cash flow sinks, you might be left holding the bag. On the other hand, if your cash flow is strong, you can repay debt fairly quickly. There is no doubt that 40 billion euros of debt sounds like a huge number, but it is more reasonable if you are bringing in 8 billion euro of EBITDA annually.

Now, it is true that all of that money cannot go toward the debt (which would wipe it out in five years), due to ongoing capital expenditure requirements. That said, Anheuser-Busch reinvests about 20% of its cash flow into the business, so they were on pace to have free cash flow of $3 billion in 2008 after reinvesting $750 million back into the business. InBev was even bigger than A-B before the merger, so free cash flow should be immense.

Assuming AHBIF reinvests 20% of operating cash flow into the business and uses the remaining 80% to repay debt, the current 40 billion euro debt load could be reduced by half within several years. At current prices, AHBIF stock could return more than 50% in 3 years, which equates to a 15% average annual return.

I have ignored taxes in this example, but fortunately the company's interest expense will wipe out much of their taxable income. To offset that variable, I also did not factor in any proceeds from asset divestitures that are likely to be completed to help with the deleveraging process. Anheuser's entertainment division (think Busch Gardens, etc) as well as their packaging division are often rumored to potentially be on the selling block. Proceeds would be used for interest and debt payments. As a result, while the numbers I have used will not prove to be exact, a net debt to EBITDA ratio of 5:1, while high, seems manageable given the strength of the combined company's business.

Note: Anheuser-Busch InBev stock trades on the Brussels exchange and recently fetched about 16 euros. Investors without access to international exchanges can buy the stock over the counter under the symbol AHBIF for around 23 dollars, but currency fluctuations will impact the dollar price, which is based on the euro quote and the prevailing exchange rate.

Full Disclosure: Peridot was long shares of Anheuser-Busch InBev at the time of writing, but positions may change at any time